Trade is global; financial tooling isn't. Brokerages don't talk to one another, or are separated by painfully slow correspondent banking rails. Opening accounts is slow and restricted by geography: if you don't happen to sit in the market with the best broker, tough luck. While trade flows across borders, the financial world doesn't. Apart from crypto, that is.

Beyond memecoins, crypto has surfaced a truly global financial system. You can buy tokenised stocks, trade perpetuals on underlying commodities, or bet on a wide spectrum of political and sporting events on prediction markets.

Initially driven by retail speculation, these on-chain venues, from DEXs like Aster and Hyperliquid to prediction markets like Kalshi and Polymarket, also offer global businesses a new way to hedge their trade flows. We covered the commodities case in our note on gold perps: because retail-heavy markets skew bullish, perpetuals often reward the opposite short view with meaningful funding rates. That suits commodity traders who hold the physical during a trade and want to offset price risk with a short on the same commodity.

But hedging on futures, perpetual or timed, is an established practice going back to the first agricultural futures on the CME. More novel are prediction markets on political events, which open up hedges that weren't possible before. These are early days and much of what's being built is experimental, but there's a clear path towards more sophisticated hedging and insurance products on top of these markets. Kalshi itself was famously inspired by the Brexit referendum: there was no way to simply bet yes or no on the outcome, only complex bundled instruments built to mimic one.

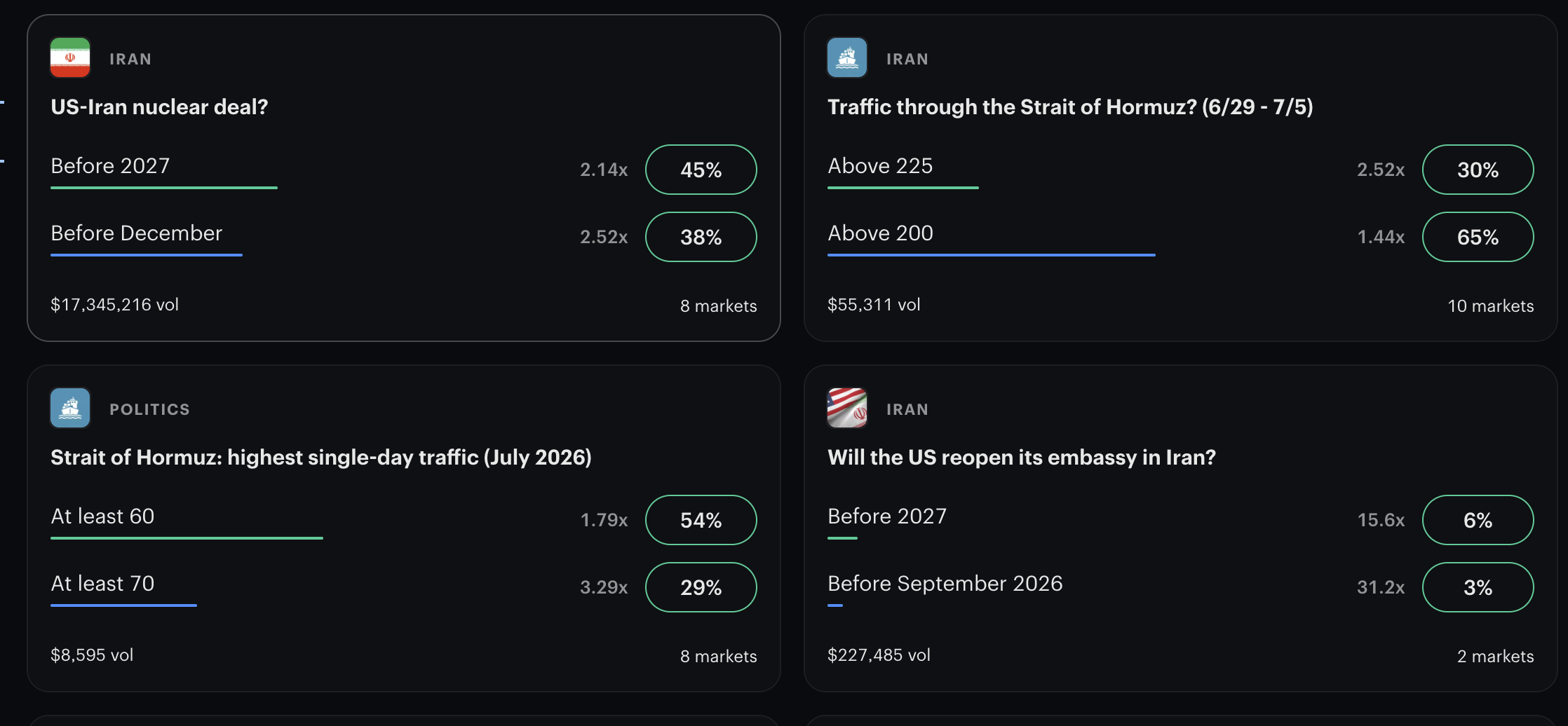

While brexit lies in the past, new political shocks are hitting trade flows. The most recent is the US/Israel/Iran war, which closed the Strait of Hormuz and disrupted trade across the GCC and well beyond. Traders shipping from Hong Kong to Dubai had orders cancelled overnight. Gold brokers couldn't ship to refineries in Dubai and re-routed to Hong Kong or Singapore, at a cost. Shipping companies had vessels stranded on the wrong side of the strait while insurers refused to cover them. Businesses were, and are, at the mercy of world events with little opportunity to hedge against them.

Both Kalshi and Polymarket, however, list a range of conflict-related markets. On Iran, Polymarket currently has the deepest: Strait of Hormuz traffic normal by July 7 (yes at 1%), by July 15 (8%), by July 31 (26%), and Iran charges Hormuz fees by August 31 (48%) and by October 31 (76%). This paints a coherent picture: traders are very confident the strait won't return to pre-war traffic in the immediate future, though that confidence wanes over time, and they're fairly confident Iran will be charging tolls by late October.

Neither bodes well for businesses shipping in and out of the Gulf. So how would a trader selling electronics from China to the UAE hedge against continued closure? We need a bet that pays out if the electronics can't actually be shipped by July 31. There's no exact fit, but the Hormuz traffic market is a decent proxy: if traffic flows normally we can ship to the UAE and earn on the trade; if it doesn't, there will be disruption. So we buy 'no' on the July 31 market. With yes at 26%, 'no' trades around 74 cents, so $50,000 buys roughly 67,500 shares. If the strait hasn't returned to normal traffic by the deadline, each share pays out $1: $67,568 in total, a 35% return that partly or fully offsets losses from the closure. If traffic does normalise, the stake is lost, but that's the world in which the goods ship and the business earns.

A few open questions remain. Not every political event has a corresponding market yet, and where one exists, liquidity isn't always deep enough to structure larger hedges or to exit when the bet turns. If 'yes' jumps from 25% to 60% on some geopolitical shift, predictors may believe it's headed to 90%, making it hard to get out and potentially making the hedge cost more than the revenue a re-opened strait would generate. Venues are already working on margined positions that would address this, letting traders swing larger with less capital at risk. Futhermore, political events don't map one-to-one to revenue: the strait resuming normal operations doesn't guarantee trade resumes, since counterparties may have moved on to traders who could ship via Fujairah in the meantime. Still, these markets offer a workable approximation of trade flow risk, and a way to put a market price on the political events that shape cross-border trade.

We also expect AI agents to play a larger role here, constructing personalised hedges across prediction and futures markets. The oil future is itself a proxy for closure, albeit a poor one, as current prices show. A basket of bets and futures, however, may well approximate the cost of an event to a business better than any single instrument.

At Nxos we're big believers in this new world of truly global finance. Businesses will look beyond classic insurance and build custom hedging products spanning perpetual futures and prediction markets. We therefore provide the bridge between off-chain and on-chain finance, letting businesses cross both worlds seamlessly and take advantage of global on-chain financial products.